.avif)

An Automation Playbook for the Modern Lending Stack: From Application to Collection

The lending industry has undergone a remarkable transformation over the past decade. What once required days of manual processing, mountains of paperwork, and countless human touchpoints can now be executed in minutes through intelligent automation. Yet many financial institutions still struggle with fragmented systems, bottlenecks, and inefficiencies that slow down their operations and frustrate customers.

The challenge is no longer digitization itself: most lenders have already invested heavily in tools and platforms. The real differentiator is how effectively those tools are orchestrated across the lending lifecycle, turning isolated automation into a cohesive, end-to-end system.

This guide walks through the complete lending lifecycle, examining each critical stage and providing a practical automation playbook to help lenders modernize their operations without sacrificing control or compliance.

The Lending Institution Tech Stack

Before diving into automation strategies, it’s essential to understand how modern lending institutions organize their technology infrastructure. The lending tech stack, at a high level, can be categorized as follows:

LayerPurposeEngagement LayerDigital acquisition (multi-channel), notifications, customer touchpointsProcess LayerLOS, LMS, workflows, orchestrationDecision LayerRules engines, AI scoring, underwriting logicData LayerDocument systems, open banking, bureaus, analyticsControl LayerCompliance, audit trails

Automation works only when these layers are loosely coupled (i.e., changes in one layer don’t break others) but tightly integrated (the layers still integrate with each other seamlessly throughout the lending lifecycle).

Stage-by-Stage Automation Playbook for Lenders

At a high level, most lenders—banks, NBFCs, fintechs, and embedded finance players—operate across six functional stages:

- Customer Acquisition

- Application & Data Capture

- Credit Assessment & Underwriting

- Decision & Approval

- Disbursement & Servicing

- Collections & Recovery

While these stages appear as a single, continuous journey from the borrower’s perspective, most lenders struggle in practice because each stage is often owned by different systems, teams, and vendors. What feels seamless to the customer actually requires significant coordination, orchestration, and integration behind the scenes. Without that alignment, automation remains fragmented→ optimizing individual steps but failing to deliver true end-to-end efficiency across the lending lifecycle.

1. Customer Acquisition

This initial stage is where potential borrowers first discover your lending products and begin their journey. Traditionally, this involved branch visits, phone calls, and manual lead qualification. Today, AI-driven conversational interfaces guide prospects through loan discovery, pre-qualification, and application initiation.

What to automate: Lead capture, initial eligibility checks, product recommendations, and application start.

The challenge: Converting interest into completed applications while collecting accurate borrower informatio1n upfront. Many lenders lose prospects due to friction in these early interactions.

The solution: Modern acquisition platforms use natural language processing to engage prospects through their preferred channels—whether web chat, WhatsApp, or SMS. By integrating directly with your CRM and loan origination systems, these tools can pre-populate application data and reduce abandonment rates.

A lightweight approach is to use a solution like Omnichannel as the front door—keeping acquisition flexible while maintaining a clean handoff to onboarding and LOS.

2. Application & Data Capture

Once a prospect decides to apply, the focus shifts to capturing complete and accurate information. This stage has historically been plagued by data entry errors, missing documents, and back-and-forth communication to fill gaps.

What to automate: Form field population, document upload and validation, OCR/IDP for income/bank statements.

The challenge: Borrowers often provide incomplete applications or submit documents in various formats. Manual review of bank statements, pay slips, and identification documents is time-consuming and error-prone.

The solution: Intelligent document processing can automatically extract data from uploaded documents, validate information against application fields, and flag discrepancies for review. Dynamic forms can adapt based on borrower responses, requesting only relevant information.

A combination of Document Management System (DMS) for structured document storage and Intelligent Document Processing (Mindox) for AI-based extraction & field-level cross-document validation creates a reliable automation layer—turning messy files into clean, decision-ready data without introducing operational fragility.

3. Credit Assessment & Underwriting

This is the heart of the lending decision—evaluating whether an applicant qualifies for credit and at what terms. Traditional underwriting relied heavily on credit bureau scores and manual analysis of financial documents, creating bottlenecks and inconsistent decisions.

What to automate: Credit bureau pulls, alternative data aggregation, risk score calculation, income/expense analysis, and initial approval/decline decisions.

The challenge: Accessing complete financial pictures of applicants, especially thin-file borrowers or small businesses. Manual underwriting creates capacity constraints and prolonged decisions.

The solution: Modern credit decisioning engines can combine traditional bureau data with alternative sources to create more comprehensive risk profiles. Machine learning models can identify patterns that traditional scorecards miss.

Solutions like Credit Scorecard Builder and Custom AI Scoring enables lenders to customize complex approval rules that enable real-time lending decisions tailored to their risk appetite.

4. Decision & Approval

Once underwriting analysis is complete, applications move through a decision workflow that may involve multiple approval tiers, exception handling, and documentation of rationale.

What to automate: Routing based on risk/amount thresholds, auto-approval for low-risk applications, task assignment for manual review

The challenge: Creating clear approval workflows that balance speed with appropriate oversight. High-value or complex applications need human judgment, while straightforward cases shouldn’t wait in queue.

The solution: Automated workflow engines can route applications based on configurable rules, escalate exceptions to appropriate reviewers, and maintain complete audit trails. Staged approval processes ensure proportionate review while keeping most applications moving quickly.

The above mentioned decision engine capabilities are among the core features of Looms (Loan Origination and Management System), which includes built-in workflow automation, task assignment, and staged approval processes that span the entire lending lifecycle.

5. Disbursement & Servicing

After approval, funds must be disbursed and the ongoing loan relationship managed. This includes payment processing, balance inquiries, and modification requests.

What to automate: Loan booking into core systems, disbursement to borrower accounts, payment schedule creation, automated payment processing and statement generation.

The challenge: Integration between origination systems and core banking platforms. Manual loan booking creates delays and data inconsistencies that impact the entire servicing lifecycle.

The solution: Straight-through processing from approval to disbursement eliminates manual handoffs and ensures data accuracy. Automated payment processing reduces operational overhead while self-service portals handle routine inquiries.

Looms (Loan Origination and Management System) handles this critical transition with disbursement capabilities through integration with third-party systems and servicing features that eliminate the gap between origination and loan management. Its integrated approach ensures that approved loans flow seamlessly into servicing workflows—with automated payment schedules, repayment tracking, collateral management, and dynamic repayment options—all within a single unified platform.

6. Collections & Recovery

When payments are missed, effective collections processes can mean the difference between recovery and write-off. Traditional collections relied on manual calling campaigns with limited visibility into borrower circumstances.

What to automate: Delinquency detection, segmentation based on risk/behavior, communication campaigns across channels, payment arrangement tracking.

The challenge: Contacting delinquent borrowers through their preferred channels, offering appropriate payment solutions, and maintaining compliance with debt collection regulations.

The solution: Modern collections platforms can automatically segment delinquent accounts, trigger personalized communication sequences, and offer self-service payment arrangement options. Integration with payment systems allows borrowers to make commitments and fulfill them without agent involvement.

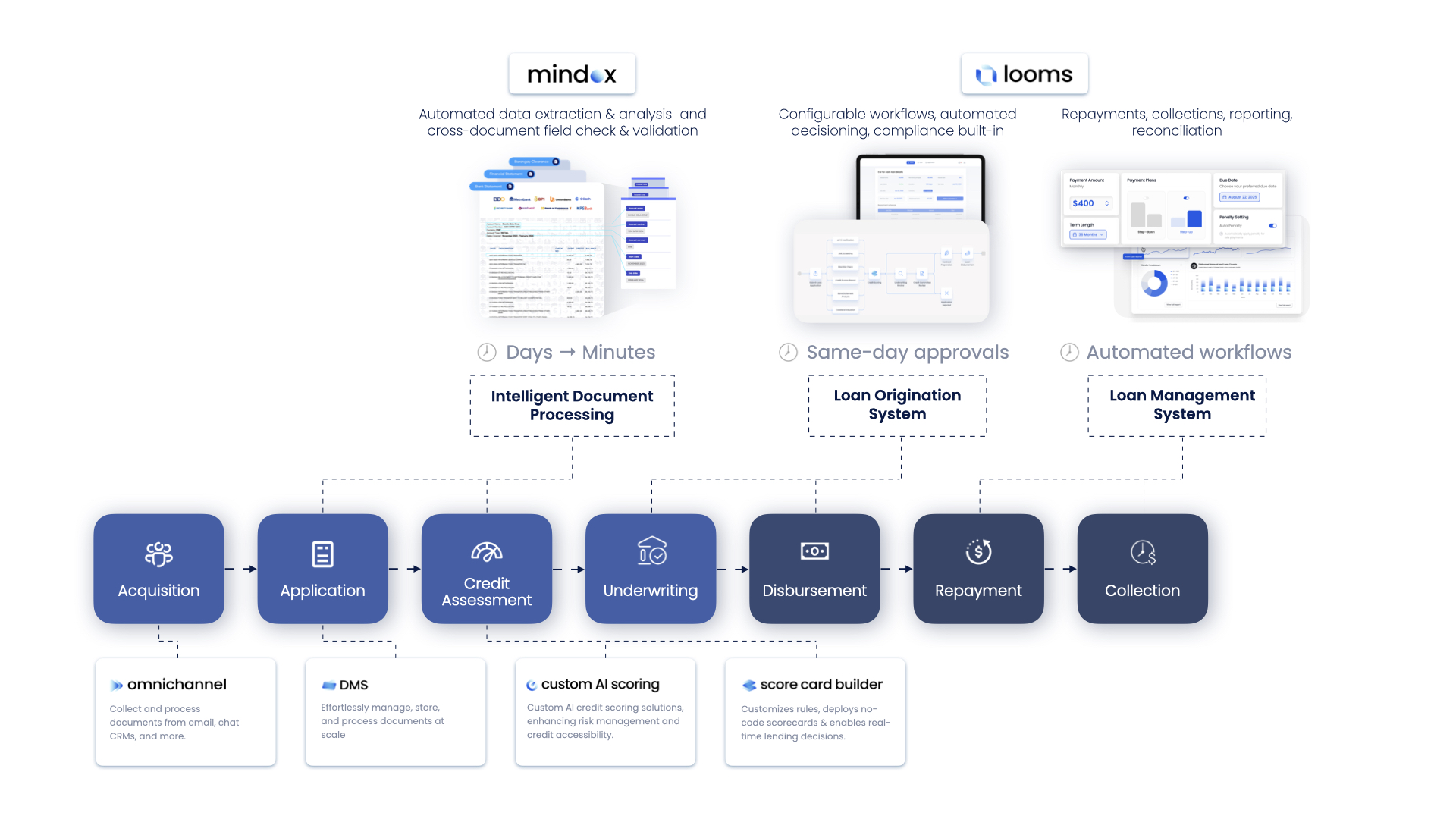

Orchestrating the Complete Lending Journey

We've explored automation opportunities at each stage of the lending lifecycle—from the moment a prospect first expresses interest through to the final collection of repayment. But in practice, these stages don't exist in isolation—they're interconnected steps in a continuous journey that must flow seamlessly from prospect to performing loan.

The illustration below brings this to life, showing how modern lenders are orchestrating their lending operations end to end—aligning core systems like LOS and LMS with intelligent layers for document management, scoring, decisioning, and omnichannel engagement.z

Measuring Success

Automation in lending only matters if it moves the needle where it counts—speed, experience, and growth.

Operational Efficiency: Time from application to decision, cost per loan originated, and the elimination of processing bottlenecks.

Customer Experience: Application completion rates, time to funding, and adoption of digital channels across borrower segments.

Business Growth: Application volume, approval rates, portfolio yield, and market expansion.

The most successful lenders establish clear baselines before implementing automation and track progress continuously. They also maintain the flexibility to adjust strategies as they learn what works in their specific market and customer segments.

In practice, this approach has already delivered measurable results for lenders working with AND Solutions:

- A leading non-bank SME lender in the Philippines, for example, transformed manual document review and credit workflows, achieving a 95% improvement in time-to-value, a 20% increase in processing capacity, and a 4× rise in employee productivity.

- A digital-first fintech streamlined its end-to-end lending lifecycle, cutting approval time from weeks to minutes, while scaling to 100,000 daily disbursements and 1.3 million daily active users.

- A pioneering rural bank streamlined its bank statement processing and credit analysis workflows, achieving 500× faster processing—from hours to under a minute—significantly reducing turnaround time and delivering an 800% productivity gain in credit review and analysis.

Conclusion: The Path Forward

Lending automation is no longer optional for financial institutions that want to remain competitive. Customer expectations, operational pressures, and market dynamics all point toward more automated, intelligent lending processes.

The key is approaching automation strategically—not as a collection of point solutions, but as an integrated capability that spans the complete lending lifecycle. By thoughtfully automating each stage while maintaining seamless data flows between them, lenders can achieve the speed and scale of digital-native competitors while preserving the risk management and compliance rigor that financial services demand.

Whether you’re a traditional bank looking to modernize legacy processes, a fintech building your infrastructure from scratch, or a non-bank lender seeking competitive advantage, the principles remain the same: automate the routine, augment human judgment where it matters most, and never stop optimizing.

Ready to modernize your lending operations? Explore our suite of lending automation solutions designed to help financial institutions automate intelligently across the complete loan lifecycle.

Related articles

.png)